For many people, the thought of receiving an inheritance seems like it would be welcome news. But depending on the size and type of the inheritance, managing the windfall can add significant complexity to one’s financial and personal life. And with analysts predicting an unprecedented wealth transfer in the U.S. in the coming years, managing the complexity of an inheritance will impact a substantial number of individuals and families.

The great wealth transfer

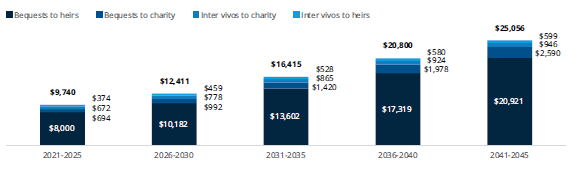

Cerulli Associates 1 anticipates approximately $84.4 trillion in wealth transfers will take place between 2021 and 2045. Additional findings from Cerulli include:

- $72 trillion in assets will be transferred to heirs, while $11.9 trillion will be donated to charities.

- $35.8 trillion (42%) of the overall total volume of transfers is expected to come from high-net-worth and ultra-high-net-worth households, which together only make up 1.5% of all households.

Wealth Transferred by Transfer Method, 2021-2045 ($ billions)

Sources: Cerulli Associates, Federal Reserve, U.S. Census Bureau, Internal Revenue Service, Bureau of Labor Statistics, and the Social Security Administration | Analyst Note: Figures in 2020 dollars. Totals represent the transfer for the five-year increment indicated (not cumulative).

PREPARING FOR THE WINDFALL

Having a proper plan in place is key to effectively managing an inheritance and helps to ensure financial security for future generations. Finding a wealth advisor experienced in the complexities of an inheritance, who can act as your “quarterback,” coordinating resources and additional legal, accounting, tax, and other professionals involved can help to make the process much smoother. Once you have your team in place, your advisor can help you determine the best options for managing your entire financial picture.

How to allocate your inheritance

While everyone’s personal circumstances are different, there are a few key options to consider when receiving an inheritance:

- Give back – An inheritance can help you advance your charitable giving goals, allowing you to give back to your community or to a cause that you care about deeply. Having a sound financial plan that identifies these goals is the first step.

- Pay down your debt – Paying down your debt can help strengthen your financial position. Not all debt is created equal, however, and not all debt is necessarily bad. Your advisor can help you determine which sources of debt to address first and how much of your inheritance is prudent to utilize.

- Save for higher education – As the costs of tuition at most U.S. universities and colleges continue to rise, if you have children, saving for higher educational expenses is likely part of your overall plan. An inheritance is an opportunity to help achieve this goal. 529s or Coverdell ESA plans are effective education savings options to consider. Each plan has distinct characteristics, and your financial advisor will work with you to identify the most appropriate option for you.

- Invest for the long term – Your financial plan should include a prudent investment strategy tailored to your goals, and receiving an inheritance should not disrupt that strategy, although your advisor can help you determine if it needs to be adjusted based on your new financial position. Ideally, a portion of your inheritance can be invested to help you reach your long-term goals even faster.

GETTING THE HELP YOU NEED

Determining what to do with your inheritance can be complicated, and you may be tempted to make “impulse buys,” or purchase non-essential luxury items. With an inheritance, it is important that you work with your financial advisor from the outset to help you determine what is best for your financial future and those of your heirs. SageSpring Wealth Partners is uniquely suited to help. More than financial advisors, we place great value on the personal side of our client relationships, seeking to provide our clients with true peace of mind throughout all life stages. We invite you to learn more by contacting one of our advisors today.